Why Personal Expenses Do Not Belong in Your Business Books

Mixing personal and business expenses may seem harmless in the moment.

You are at the store. You buy office supplies, a few household items, groceries, and maybe something for the kids. You swipe the business card because it is the one in your hand. You tell yourself, “I’ll clean it up later.”

Maybe you will.

But here is the problem: mixing personal and business expenses does not just create a tax headache. It can weaken the legal separation between you and your business.

Most small business owners hear the same warning over and over: “Do not mix personal and business expenses because the IRS might audit you.”

That is true, but it is not the whole story. And frankly, it may not be the biggest risk.

The IRS explains that an audit is a review of accounts and financial records to confirm that information reported on a tax return is correct. The IRS may select returns through computer screening, random selection, or because the return is linked to another taxpayer under examination.1

So yes, clean records matter for tax purposes. But fear of audits should not be the only reason business owners care about clean books.

The stronger reason is this:

If you do not treat your business like a separate business, someone else may argue that it should not be treated separately either.

That is where the legal concept of “piercing the corporate veil” comes in.

What Is the Corporate Veil?

If you formed an LLC or corporation, one of the main reasons was probably liability protection.

In plain English, the business is supposed to be separate from you personally. The business has its own money, its own obligations, its own contracts, and its own records. If something goes wrong, the general idea is that business debts and claims stay with the business.

That separation is often called the “corporate veil.”

Cornell Law School’s Legal Information Institute explains that piercing the corporate veil allows a court, in certain situations, to disregard the separate legal identity of a business entity and hold shareholders or owners personally responsible. Cornell also notes that courts generally presume against piercing the veil, but may do so when the company is merely the owner’s alter ego or when respecting the separate entity would promote fraud or injustice. 2

That is the key point: liability protection is not magic. You have to respect the separation.

Why Commingling Funds Matters

Commingling means mixing personal and business money or assets together.

Cornell Law School identifies commingling funds or assets as one of the factors courts may consider when deciding whether to disregard the corporate entity. Other factors may include failure to maintain proper records, failure to follow corporate formalities, and undercapitalization. 3

Examples of commingling may include:

· Personal bills paid from the business account.

· Business income deposited into a personal account.

· A business debit card used for groceries, clothing, family expenses, or personal shopping.

· Personal credit cards are used regularly for business expenses without clear reimbursement records.

· Owner draws or distributions taken randomly with no documentation.

· Personal purchases buried inside business expense categories.

One mistake does not automatically destroy your liability protection. Real life happens. A single accidental swipe on the wrong card is not the same thing as treating the business account like a personal wallet.

But repeated sloppy habits can become evidence. And in a legal dispute, evidence matters.

The Bigger Risk May Not Be the IRS

No one wants an IRS audit. But for many small businesses, fear of audits may be less immediate than fear of legal exposure.

The U.S. Chamber Institute for Legal Reform reported that small businesses carried an estimated $160 billion in commercial tort costs in 2021. The same research stated that businesses with $10 million or less in annual revenue accounted for only 20% of commercial revenues but bore 48% of commercial tort costs. 4

That does not mean every small business will be sued. But it does mean lawsuits, claims, disputes, and creditor issues are not imaginary risks.

If your business is ever involved in a legal claim, a creditor dispute, a vendor issue, an employee claim, or a customer complaint, someone may look at how the business was operated. If your books show that personal and business money were routinely mixed together, you may have handed them a useful argument.

Wolters Kluwer, through its CT Corporation resources, warns that owners of LLCs and corporations need to respect the business entity’s separate existence. It specifically discusses the risk of piercing the veil when business owners fail to keep proper separation between themselves and the entity.5

In other words, the issue is not just, “Can I deduct this?”

The better question is: Am I treating this business like it is truly separate from me?

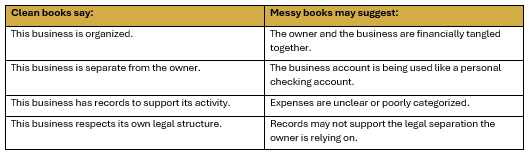

Your Books Tell a Story

Your bookkeeping is not just a tax-season chore. Your books tell a story about how your business operates.

That second story is not the one you want told in a dispute.

“But I Own the Business. Isn’t the Money Mine Anyway?”

Not exactly.

If you are a sole proprietor, you and the business are generally not legally separate in the same way, and an LLC or corporation may be. Even then, clean bookkeeping still matters because it helps track income, expenses, taxes, profit, and cash flow.

If you operate through an LLC or corporation, separation matters even more.

Yes, you may own the company. But the company’s money should not be treated like your personal checking account.

You can pay yourself. You can take owner’s draws or distributions when appropriate. You can reimburse yourself for legitimate business expenses. But those transactions should be recorded clearly and consistently.

There is a big difference between:

Owner distribution is recorded properly in the books.

And:

Business debit card used for groceries, Target runs, kids’ clothes, dinner, Amazon orders, and then buried under office supplies.

The first one is bookkeeping. The second one is chaos with a debit card.

How to Keep Personal and Business Expenses Separate

The solution does not have to be complicated. It does, however, need to be consistent.

Start with the basics:

· Open a separate business checking account.

· Use a dedicated business credit card.

· Avoid paying personal bills from the business account.

· Avoid depositing business income into personal accounts.

· Record owner draws, distributions, and reimbursements properly.

· Keep receipts and documentation.

· Review your books regularly, not just at tax time.

· Do not hide personal expenses inside business categories.

· Ask your bookkeeper or accountant how to properly record accidental personal purchases.

If you accidentally use the business card for something personal, do not panic. Just do not pretend it was a business expense. Record it properly.

Clean books are not about perfection. They are about transparency.

The Real Reason This Matters

Keeping personal and business expenses separate is not just about avoiding an IRS audit.

It is about protecting the structure you created.

If you formed an LLC or corporation, you likely did it for a reason. You wanted professionalism, credibility, organization, and liability protection. But those benefits are stronger when your financial habits support them.

When you treat the business like a real business, your records help support that position.

When you treat the business account like your personal wallet, your records may undermine it.

That matters.

Bottom Line

The IRS matters. Taxes matter. Deductions matter.

But the bigger issue is this: separating personal and business expenses helps protect the legal and financial boundary between you and your business.

Your bookkeeping should not only answer, “Can I deduct this?”

It should also answer the question, “Am I respecting the separation between myself and my business?”

That is the standard worth paying attention to.

Clean books are not just about compliance. They are about protecting what you are building.

Citations

1. Internal Revenue Service, IRS Audits, IRS.gov, https://www.irs.gov/businesses/small-businesses-self-employed/irs-audits (last visited May 17, 2026).

2. Legal Information Institute, Cornell Law School, Piercing the Corporate Veil, Wex, https://www.law.cornell.edu/wex/piercing_the_corporate_veil (last visited May 17, 2026); Legal Information Institute, Cornell Law School, Alter Ego, Wex, https://www.law.cornell.edu/wex/alter_ego (last visited May 17, 2026).

3. Legal Information Institute, Cornell Law School, Disregarding the Corporate Entity, Wex, https://www.law.cornell.edu/wex/disregarding_the_corporate_entity (last visited May 17, 2026).

4. U.S. Chamber Institute for Legal Reform, New U.S. Chamber Study Shows Lawsuit System Costs Small Businesses $160 Billion, InstituteForLegalReform.com (Feb. 14, 2023), https://instituteforlegalreform.com/press-release/new-u-s-chamber-study-shows-lawsuit-system-costs-small-businesses-160-billion/. The report summarizes findings from The Brattle Group, Tort Costs for Small Businesses.

5. Wolters Kluwer, Piercing the Corporate Veil: LLC & Corporation Risks, WoltersKluwer.com, https://www.wolterskluwer.com/en/expert-insights/piercing-the-veil-of-small-business-what-the-owners-of-llcs-and-corporations-need-to-know (last visited May 17, 2026).

Additional Sources and Fun Reading

Internal Revenue Service, Audits Records Request, IRS.gov, https://www.irs.gov/businesses/small-businesses-self-employed/audits-records-request (last visited May 17, 2026).

Internal Revenue Service, SOI Tax Stats, 2023 IRS Data Book Table 17 (Revised), IRS.gov, https://www.irs.gov/statistics/soi-tax-stats-2023-irs-data-book-table-17-revised (last visited May 17, 2026).

Legal Information Institute, Cornell Law School, Piercing the Veil, Wex, https://www.law.cornell.edu/wex/piercing_the_veil (last visited May 17, 2026).

Legal Information Institute, Cornell Law School, Commingling, Wex, https://www.law.cornell.edu/wex/commingling (last visited May 17, 2026).

Wolters Kluwer, How to Avoid Piercing the Corporate Veil, WoltersKluwer.com, https://www.wolterskluwer.com/en/expert-insights/how-to-avoid-piercing-the-corporate-veil (last visited May 17, 2026).

Wolters Kluwer, Leveraging Limited Liability for Personal Asset Protection, WoltersKluwer.com, https://www.wolterskluwer.com/en/expert-insights/leveraging-limited-liability-for-asset-protection (last visited May 17, 2026).

The Brattle Group, Tort Costs for Small Businesses, Brattle.com, https://www.brattle.com/insights-events/publications/tort-costs-for-small-businesses/ (last visited May 17, 2026).

This article is written from a bookkeeping and business records perspective. It should not be presented as legal advice or tax advice. Business owners should consult an attorney or tax professional about their specific entity, state law, and circumstances.